Sales and working capital are directly proportional to each other. One strategy is to match the maturity of the finance with the life of the asset being financed. This strategy minimises the risk that the firm will be unable to meet its maturing obligations.

An example would be if a firm uses a 2-year loan to finance property, plant and equipment which is expected to have a useful life of 5 years. This means that after two years the loan is due to be paid, meaning that the asset financed would have not yet generated enough cash flows that are required to repay the loan.

With working capital, the company should ensure that they finance the investment in current assets with finance that matures almost at the same time as the finance used to fund it.

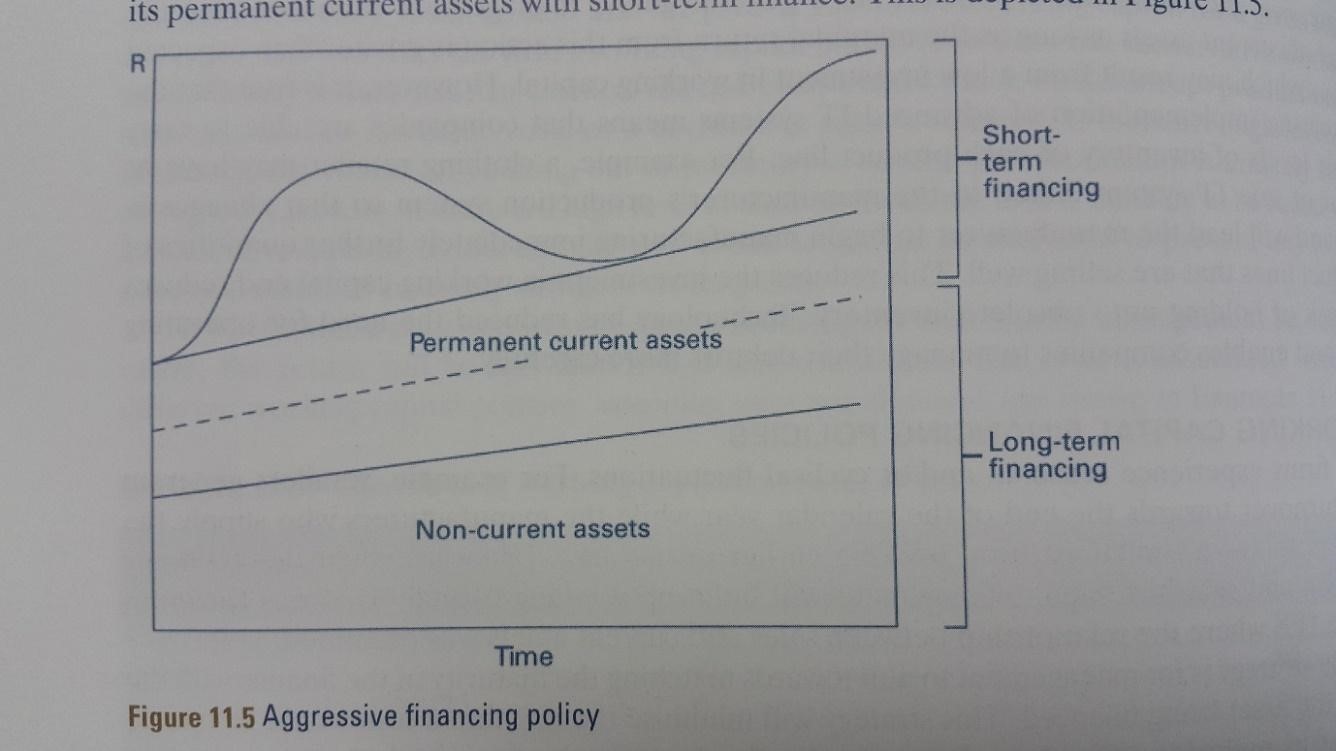

Figure 5.6 Aggressive Approach to working capital financing

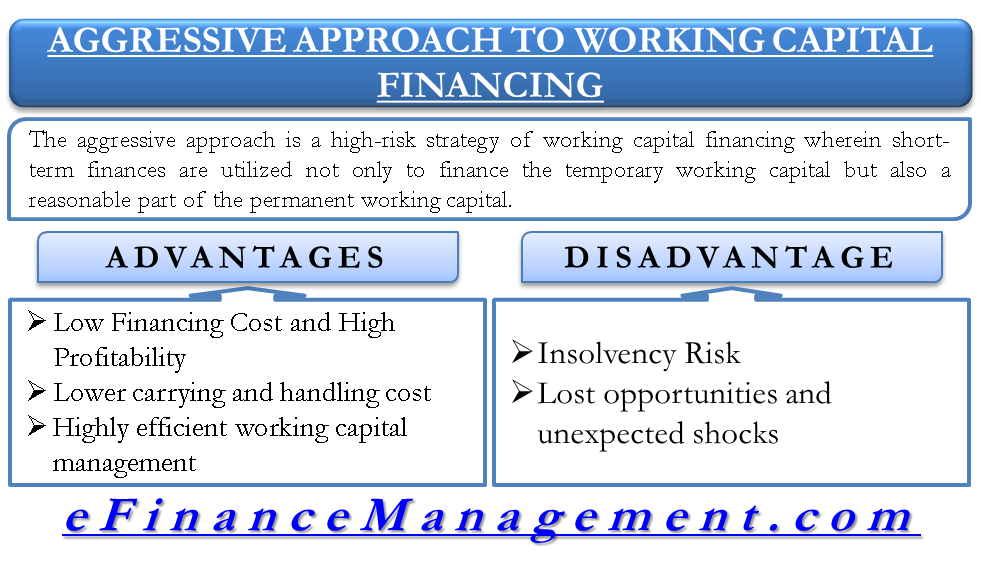

In an aggressive policy the dotted line in the figure below could lie between the line designating non-current assets which indicates that all the current assets plus part of the non-current assets are paid for by short-term financing.

Figure 5.7 Aggressive Working Capital Policy Graph

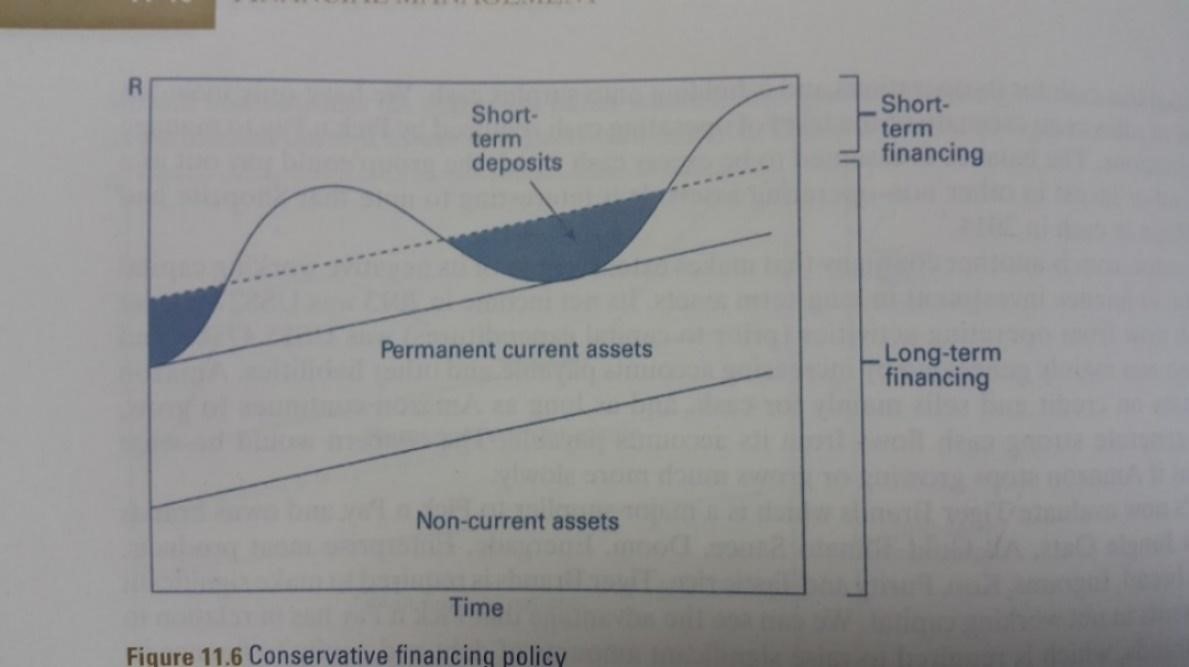

In a conservative policy the long-term finance is used to finance both permanent and some portion of fluctuating current assets, however it would generate the lowest return because the cost of long-term finance will be higher than that earned on short-term deposits.

Figure 5.8 Conservative Working Capital Policy Graph