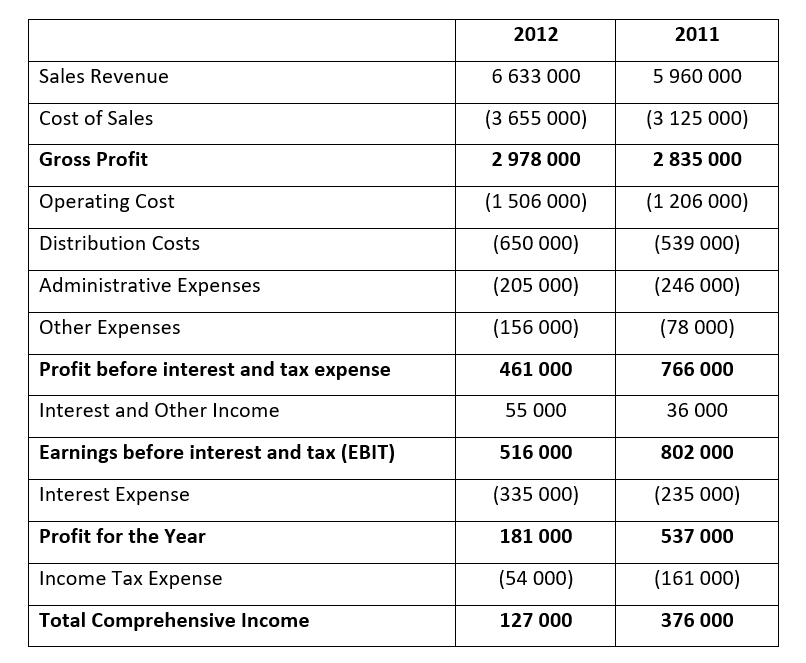

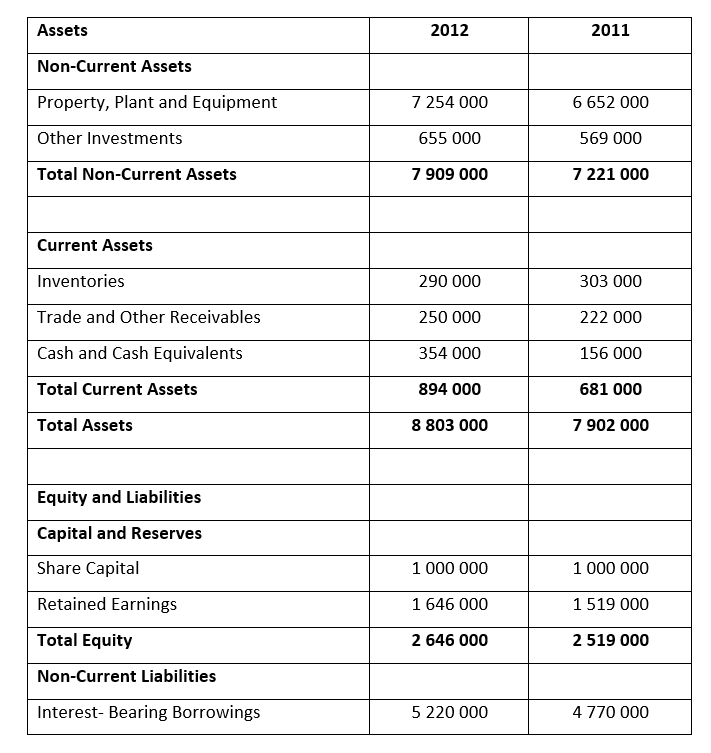

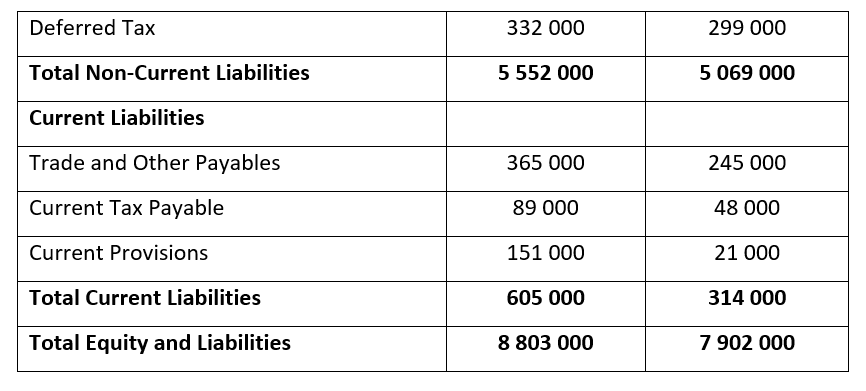

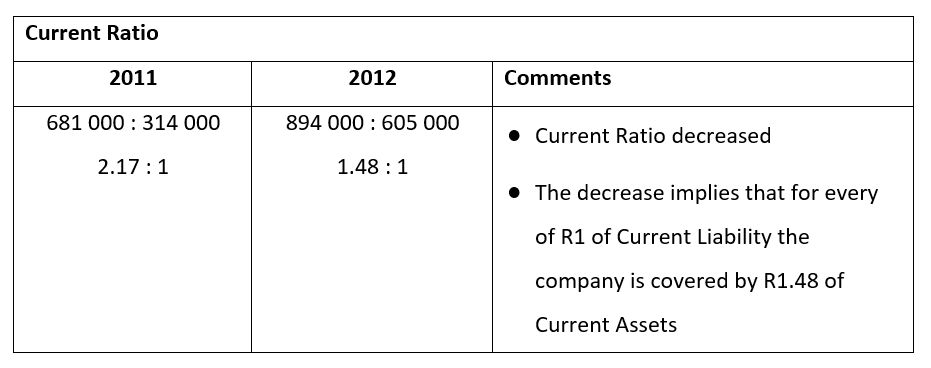

4.6 Example 1

Tasks

Having understood the above, apply yourself in answering the following for the two respective years:

Having understood the above, apply yourself in answering the following for the two respective years: